Reorder Point – What Is It and How Do I Use It?

The Big Picture

Keeping track of inventory might sound pretty boring, but trust me, it’s more important than you think. This is especially important for retailers. Good inventory management is about striking a balance—enough stock to keep your customers happy but not so much that all your cash is tied up and you’re drowning in unsold goods with no cash to pay the water bill.

You see, for those of us who aren’t aware, inventory is basically cash, but locked in a lockbox that can only be opened with the sale of a product. So, if you are deciding to lock up your cash in the form of inventory sitting on shelves, you better have a very solid understanding of when that lockbox will release its green treasure inside. Otherwise, you’re locking up that value for no good reason. Trust me when I tell you that uncontrolled inventory levels will kill a business.

In a recent engagement with a small retail store client, managing their inventory was a major issue. They simply didn’t understand:

- Why it was so important nor

- How to do it.

Yes, they understood as a general concept that managing inventory was important, but they didn’t fully appreciate how its mismanagement had downstream affects (until those affects hit like a Florida hurricane). Their understanding of ‘inventory management’ only extended to understanding the need to have inventory on the shelves for customers to buy in the moment. It did not extend to understanding the downstream effects of inefficient inventory levels.

And this brings us to the first topic in a series of three essays over the coming weeks about inventory management: Reorder Point.

Reorder Point answers the fundamental question,

When Do I Reorder?

You’re In the Inventory Management Business

You Think You Can Eyeball This?

For that small retail establishment, not understanding inventory management was, by far, their biggest problem. If you don’t know why doing a thing is important, you’ll never bother learning how to do it properly.

To fix this issue, I started by changing their thinking: I told them that they weren’t in the widget-selling business; they were in the inventory management business. No matter what their store was selling, they must always ensure their inventory levels were optimized. This new way of thinking means that we all must be experts in managing our inventories.

And what does that mean? It means efficiently managing inventory across three components:

- Reorder Point

- Safety Stock

- Economic Order Quantity

We’ll be discussing these three aspects to inventory management over the coming weeks, but this week, we’re talking about Reorder Point.

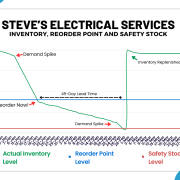

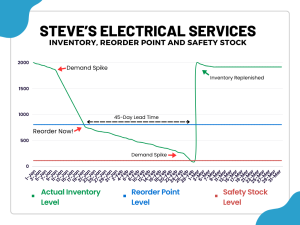

What is a Reorder Point?

The reorder point (RP) is the level of inventory that, when your inventory levels drop to that count, you place a new order. It helps you restock before running out, keeping customers happy and cash flow in check.

The Big Picture

Steps to Set Reorder Points:

1. Calculate Your Average Daily Demand:

First things first, you need to know how much you sell each day. Don’t guess; use your sales data. Look at a month or two, count how many units you sold, and divide by the number of days. For example, if you sold 300 units in 30 days, that’s 10 units per day. Easy math, right? And don’t be afraid of fractions of a unit. We’re doing math to calculate averages here so fractions are permissible.

2. Determine Your Lead Time:

Next, figure out your lead time. That’s a fancy way of saying,

“How long does it take for the stuff I ordered to show up at my door?”

If your supplier typically takes 7 days to deliver, then that’s your lead time. Just make sure you’re not counting on that one magical day when everything showed up in 24 hours! We’re looking for typical, average lead times.

3. Add Some Safety Stock:

We’re going to talk about Safety Stock, what it is and how to calculate it, next week. But for now, just understand that this is your emergency stash. It’s that extra roll of toilet paper you hide in the back of the closet. Safety stock is there to protect you against the unexpected—like if demand suddenly spikes or your supplier goes on vacation. If you’re selling consistently, you might not need much. If your sales are all over the place, stock up a bit more. As I said, we’ll discuss how to calculate Safety Stock next week.

4. Calculate Your Reorder Point:

Now, here’s where the magic happens. The formula for RP is simple:

Reorder Point = (Average Daily Demand × Lead Time) + Safety Stock.

For example, if you sell an average of 10 units a day, your lead time is 7 days, and you keep 20 units as safety stock, your reorder point is

(10 × 7) + 20 = 90 units.

In practice, what this means is that when your inventory level drops to 90 units, you start calling your vendor to place an order. And yes, it truly is that simple.

Now, contrast this to the bad old days of inventory management by just walking around and eyeballing your inventory. You’d look at your shelves, notice that you’re a little low on some widget or doohickey and you put in an order to replenish. Who knows if you actually needed that doohickey. But it looked low so you put in an order, tying up yet more cash into that lockbox.

When you set data-driven reorder points, you’re taking control. No more guessing games. You’ll know exactly when it’s time to reorder, keeping your shelves stocked and your customers smiling.

The Catch

But there’s a catch! This absolutely presumes that you have the data (or can estimate it) to run these calculations. This means then that, if you want to take your inventory management to the next level and move beyond merely eyeballing and unnecessarily locking up cash, you need to keep track of the relevant variables. This is yet another reason to keep good records and manage your business with data and not hunches.

So there you have it: Reorder Point. It is the inventory count that, when your inventory levels drop to this number, it is time to reorder. It takes an objective, mathematical and data-driven approach to managing your inventory that takes the guess work out of things and guarantees an efficient use of your limited funds.

The Shameless Plug

![]() If you’re thinking that you’d like some assistance in getting your inventories organized and optimized, or if you’re thinking that your business in general is not running as efficiently as you believe it could be, please schedule a zoom call to discuss what’s on your mind. I am 100% confident that whatever issue or pain point you are facing, I have seen it before and have a solution ready – made for you.

If you’re thinking that you’d like some assistance in getting your inventories organized and optimized, or if you’re thinking that your business in general is not running as efficiently as you believe it could be, please schedule a zoom call to discuss what’s on your mind. I am 100% confident that whatever issue or pain point you are facing, I have seen it before and have a solution ready – made for you.

- Inventories out of control? There’s a solution.

- Accounting completely incomprehensible? We can fix that too.

- Business processes inefficient and costing you money? Completely solvable.

So please, don’t hesitate to reach out. I offer a free 1-hr consult to discuss your issues and create a plan to tackle it.

Every business needs an annual check up.

The 5D Business Check Up measures your business across the 5 major dimensions common to every business:

The 5D Business Check Up measures your business across the 5 major dimensions common to every business:

-

Sales & Marketing

-

Finance & Accounting

-

Operations

-

Inventory Management

-

Strategy & Planning

The 5D Business Check up starts with over 40 questions that delves into your personal observations as well as objective measurements taken directly from your financial statements. Once your questionnaire is complete, you will recieve a formal report assessing the strengths and weaknesses of your business with recommendations to improve.

Purchase the 5D Business Check Up here

Thinking About Starting a Business?

Learn the skills and get the knowledge you need to start, operate and manage your business efficiently with The Tradesman’s MBA. You can learn more about this great resource for the entreprenuer here.

In the world of small business, a business model is like the architectural blueprint of a building. It lays out how a company intends to operate, generate revenue, and sustain itself in the long run. A well-defined business model is important because it helps entrepreneurs understand their market, allocate resources efficiently, and communicate their value proposition to stakeholders.

In the world of small business, a business model is like the architectural blueprint of a building. It lays out how a company intends to operate, generate revenue, and sustain itself in the long run. A well-defined business model is important because it helps entrepreneurs understand their market, allocate resources efficiently, and communicate their value proposition to stakeholders.

You see, my friend and his son didn’t buy a business with employees; he and his son are the employees. What this means is that because they have so much work to do, they don’t have time for much else. As soon as the purchase of the business closed, they have been running at a million miles an hour trying to keep up with the work they have booked! When last I spoke with him, he had jobs booked out at least a month and a half into the future. A very good problem to have. But because he and his son are the only employees, their business will never grow beyond what they can do. At a certain point, Queue Theory states that their future customers will cease waiting in line and hop to a competitor! Not good.

You see, my friend and his son didn’t buy a business with employees; he and his son are the employees. What this means is that because they have so much work to do, they don’t have time for much else. As soon as the purchase of the business closed, they have been running at a million miles an hour trying to keep up with the work they have booked! When last I spoke with him, he had jobs booked out at least a month and a half into the future. A very good problem to have. But because he and his son are the only employees, their business will never grow beyond what they can do. At a certain point, Queue Theory states that their future customers will cease waiting in line and hop to a competitor! Not good. One day my friend and I were chatting and he told me about a job that they had just finished. He proudly told me that it priced out to a tune of $15,000; a princely sum no matter who you are. I naturally congratulated him on booking such a high-priced job and asked, “How did the costs break out for that $15,000 dollar job?” I was obviously curious about the margin of such a high-priced job.

One day my friend and I were chatting and he told me about a job that they had just finished. He proudly told me that it priced out to a tune of $15,000; a princely sum no matter who you are. I naturally congratulated him on booking such a high-priced job and asked, “How did the costs break out for that $15,000 dollar job?” I was obviously curious about the margin of such a high-priced job. These four steps would pay HUGE dividends in operational efficiency for his company. And efficiency, as a business owner, should be what you are aiming for. Not just ‘high priced’ jobs. How well are you managing your operations?

These four steps would pay HUGE dividends in operational efficiency for his company. And efficiency, as a business owner, should be what you are aiming for. Not just ‘high priced’ jobs. How well are you managing your operations?